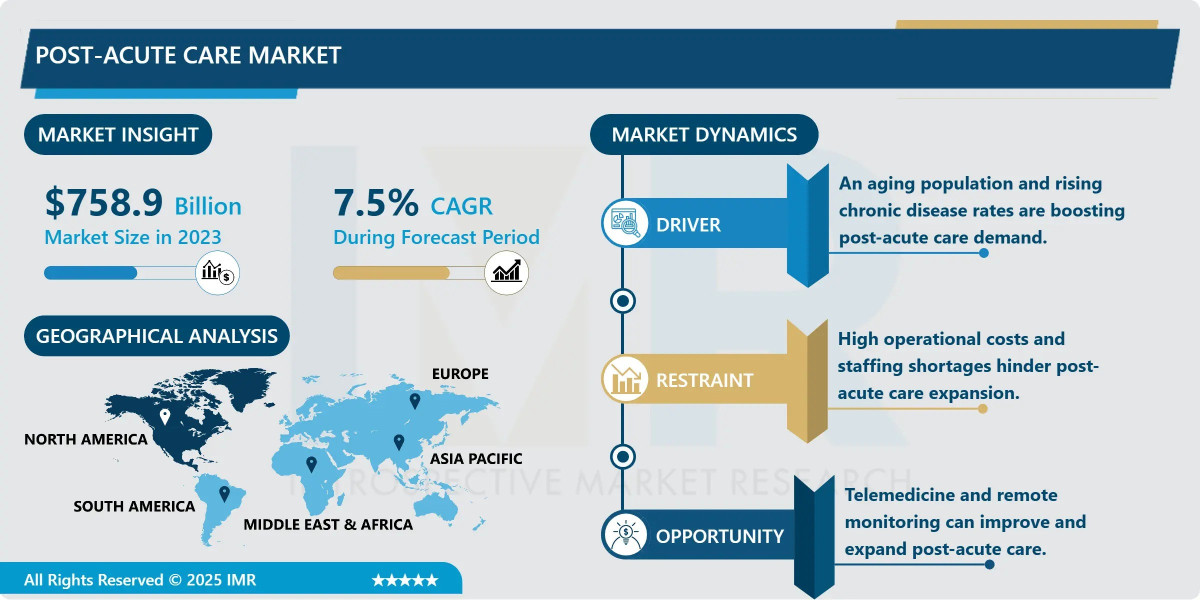

According to a new report published by Introspective Market Research, Post-acute Care Market by Service, Age Group, Condition, and Region, The Global Post-acute Care Market Size Was Valued at USD 758.9 Billion in 2023 and is Projected to Reach USD 1,455.0 Billion by 2032, Growing at a CAGR of 7.5%.

Overview:

The global post-acute care market encompasses a continuum of medical and supportive services provided to patients following an acute care hospital stay. This market includes settings such as skilled nursing facilities (SNFs), inpatient rehabilitation facilities (IRFs), long-term care hospitals (LTCHs), and home health agencies. The key advantage of specialized post-acute care over an extended general hospital stay is its focus on recovery, rehabilitation, and functional improvement in a more cost-effective setting. These services help patients regain independence, manage chronic conditions, and prevent hospital readmissions by providing tailored therapeutic interventions, nursing care, and assistance with daily living activities.

Post-acute care is a critical component of the healthcare ecosystem, serving a diverse patient population across major demographic segments. Its primary uses include rehabilitation for patients recovering from major surgeries (e.g., joint replacements, cardiac procedures), strokes, or serious injuries; management of complex chronic illnesses like heart failure and COPD; and long-term custodial care for the elderly or disabled. The market serves an aging global population, patients with disabilities, and individuals requiring transitional care, making it an essential link between hospitalization and a return to community living.

Growth Driver:

The paramount growth driver for the post-acute care market is the rapid global aging of the population, particularly the expansion of the cohort aged 65 and older. This demographic shift is creating an unprecedented and sustained demand for healthcare services tailored to age-related conditions. Older adults have higher rates of chronic diseases (such as diabetes, arthritis, and dementia), experience more frequent acute medical events (like strokes and fractures), and often require prolonged recovery and rehabilitation. This demographic inevitability directly fuels demand for skilled nursing, rehabilitative therapy, and long-term supportive care services. As life expectancy increases, the need for post-acute care that maximizes functional independence and quality of life for the elderly becomes a critical and growing component of national healthcare systems worldwide.

Market Opportunity:

A significant market opportunity lies in the integration of technology and value-based care models to create more efficient, patient-centric, and home-based post-acute care solutions. The shift towards value-based reimbursement incentivizes providers to prevent costly hospital readmissions and improve patient outcomes. This creates demand for remote patient monitoring (RPM) technologies, telehealth platforms, and data analytics to manage patients proactively at home. Furthermore, there is immense potential in developing specialized, high-acuity home health programs that can safely deliver complex nursing and rehabilitation services outside of facility walls, appealing to patient preference and offering cost advantages. Companies that successfully blend high-touch clinical care with high-tech monitoring and data-driven care coordination will lead the next phase of market evolution.

Post-acute Care Market, Segmentation

The Post-acute Care Market is segmented on the basis of Service, Age Group, and Condition.

Service

The Service segment is further classified into Skilled Nursing Facilities, Inpatient Rehabilitation Facilities, Long-term Care Hospitals, and Home Health Care. Among these, the Skilled Nursing Facilities sub-segment accounted for the highest market share in 2023. SNFs dominate as they provide the most common and comprehensive level of post-hospital care, offering 24/7 nursing, rehabilitative therapies (physical, occupational, speech), and medical supervision for patients who are not yet ready to return home but no longer require acute hospital care. Their role as the workhorse of the post-acute continuum, especially for the elderly, solidifies their leading position.

Age Group

The Age Group segment is further classified into Elderly (65+), Adults (18-64), and Children. Among these, the Elderly (65+) sub-segment accounted for the highest market share in 2023. The elderly population is the primary consumer of post-acute care services due to their higher prevalence of chronic conditions, increased vulnerability to acute illnesses and injuries, and greater need for rehabilitation and long-term support after hospitalization. This demographic's growth is the single most powerful driver of demand across all post-acute care settings.

Some of The Leading/Active Market Players Are-

• Encompass Health Corporation (US)

• Kindred Healthcare, LLC (A LifePoint Health Company) (US)

• Genesis Healthcare, Inc. (US)

• Amedisys, Inc. (US)

• LHC Group, Inc. (A UnitedHealth Group/Optum Company) (US)

• Select Medical Holdings Corporation (US)

• BAYADA Home Health Care (US)

• Brookdale Senior Living Inc. (US)

• Sonida Senior Living, Inc. (US)

• The Ensign Group, Inc. (US)

• Saber Healthcare Group (US)

• Trilogy Health Services, LLC (US)

• ProMedica Senior Care (US)

• Sunrise Senior Living, LLC (US)

• “and other active players.”

Key Industry Developments

News 1:

In April 2024, Encompass Health announced a major expansion of its home health and hospice segment, investing in new technology for remote therapeutic monitoring and predictive analytics.

The initiative aims to improve outcomes for patients transitioning from its inpatient rehabilitation hospitals to home care, reducing readmission rates and capturing more of the care continuum.

News 2:

In March 2024, the U.S. Centers for Medicare & Medicaid Services (CMS) introduced new payment models designed to better coordinate care between hospitals and post-acute care providers.

This regulatory shift is accelerating partnerships and mergers between health systems and post-acute providers to create integrated networks that can share risk and improve patient transitions.

Key Findings of the Study

• Skilled Nursing Facilities are the dominant service type, and the Elderly (65+) population is the leading age group.

• North America holds the largest market share, driven by a well-established reimbursement system (Medicare), a large aging population, and high healthcare expenditure.

• The rapidly aging global population is the primary market growth driver.

• Key trends include the expansion of home-based care models, integration of technology for remote monitoring, and industry consolidation to form integrated care networks.